In Part 1, I wrote about why crashes feel the way they do — the psychology of panic, the history of markets that fell and recovered, and why your brain will betray you exactly when you need it most.

But here's the thing: understanding why you panic doesn't stop you from panicking. I know loss aversion is irrational, and I still feel the gut punch when my portfolio drops 20%. Knowing the theory helps — a little. What helps a lot more is having a system in place that works even when your judgment doesn't.

That's what this article is about. Less theory, more plumbing.

The Best Time to Build a Lifeboat Is Before the Storm

Most people think about crash survival during a crash. By then, your options are limited and your thinking is compromised.

The real work happens long before the first red day. It happens when you choose your asset allocation, set up your SIPs, and decide the rules you'll follow — before fear has any say in the matter.

Think of it like a fire escape plan. You don't design it while the building is on fire. You design it on a calm Tuesday afternoon, write it down, and follow it without thinking when the alarm goes off.

Everything in this article is a calm Tuesday afternoon kind of decision.

Asset Allocation: The Thing That Actually Saves You

When a crash hits, the first thing that determines how much pain you feel isn't which funds you own — it's how your money is split between equity and debt.

Two people I know — similar salaries, similar SIP amounts. One had 100% in equity. The other had a 60/40 equity-debt split. Same crash. The first person lost sleep, stopped SIPs, and eventually sold near the bottom. The second person felt the pain — of course they did — but the debt cushion kept their overall losses manageable enough that they stayed put. Three years later, the second person was significantly ahead. Not because they picked better funds. Because their portfolio was built to survive them.

This is why I keep saying asset allocation matters more than stock selection, fund selection, or any other decision you'll make. It determines both your returns and your ability to stay invested — and the second one matters far more than most people realize.

Where you sit on the map depends on two things:

Your time horizon — how long until you need the money. And your risk capacity — honestly, how much volatility you can absorb without doing something destructive.

| Time Horizon | Risk Capacity | Suggested Split |

|---|---|---|

| 15+ years, stable income | High | 70-100% equity, rest in debt |

| 10-15 years, moderate income | Moderate | 50-75% equity, 25-50% debt |

| 5-10 years, or nearing goal | Lower | 30-50% equity, 50-70% debt |

| Under 5 years | Low | Mostly debt, minimal equity |

The common mistake is overestimating your risk capacity during bull markets. When everything is green and your portfolio is up 25%, "100% equity" feels obvious. When that same portfolio is down 40%, it feels insane.

Your real risk tolerance is whatever lets you sleep at night during a 40% drawdown and still not touch your investments. If you haven't experienced that, be conservative. You can always increase equity later. Coming back after panic-selling is much harder.

If You're New: Start Conservative, Then Build

This one's specifically for people who haven't been through a real crash yet.

I know what you're thinking. "I'm young, I have a long horizon, I should go 100% equity for maximum returns." On paper, you're right. In practice, I've watched this story end badly too many times. You go all-in, markets drop 30% in your first year, and you bail — converting what should have been a temporary dip into a permanent exit from equity investing.

Here's what I'd suggest instead: start with an aggressive hybrid fund. Roughly 65-75% equity, 25-35% debt. You still get most of the equity upside, but the debt cushion means your first correction feels like a -15% dip instead of a -30% freefall. That's a very different emotional experience. One you can learn from without being scarred by.

Think of it as learning to swim in the shallow end. You won't stay there forever — you're there to learn that water holds you up, so that when you eventually go deeper, you don't drown.

After 2-3 years, once you've lived through at least one meaningful correction and understand how you actually react — not how you imagine you'd react, but how you actually behave when money is disappearing — you can shift to a more aggressive allocation if your goals support it.

There's no shame in starting conservative. The people who stay invested for 15 years with a moderate allocation will almost always outperform the ones who went all-in on equity and bailed after their first crash.

Rebalancing: The Boring Habit That Quietly Protects You

I want to talk about something that sounds incredibly dull but is one of the most underrated tools in a crash survival kit: periodic rebalancing.

Here's the core idea. You set a target allocation — say 50% equity, 50% debt. Over time, markets move, and that split drifts. After a strong rally, equity might swell to 65% of your portfolio. After a crash, it might shrink to 35%. Rebalancing simply means bringing it back to 50/50. That's it. You're not predicting anything. You're not timing anything. You're just maintaining the split you chose on a calm day.

The point of rebalancing is to keep your portfolio honest. Left alone, a portfolio drifts — sometimes aggressively. After a long bull run, you might find yourself at 75% equity when you signed up for 50%. That means you're carrying far more risk than you intended, right when a correction is statistically more likely. Rebalancing brings you back to the plan.

Rebalancing has nothing to do with predicting what markets will do next. You're not trying to time rallies or buy dips. You're simply maintaining the risk level you chose when your thinking was clear. The discipline is in the consistency, not the timing.

The real benefit shows up in how much less you lose during the bad stretches.

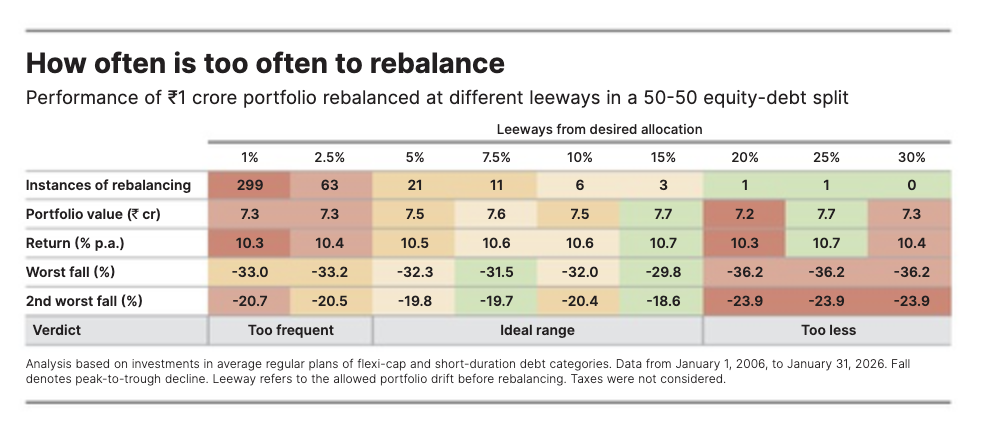

Value Research ran a detailed analysis across every major market cycle from 2006 to 2026, testing how much leeway to allow before rebalancing a 50:50 equity-debt portfolio:

Source: Value Research. Performance of ₹1 crore invested in average regular plans of flexi-cap and short-duration debt categories. Data from January 1, 2006 to January 31, 2026. Taxes were not considered.

Look at the returns column first. Across every rebalancing frequency — from obsessive (1% leeway, 299 rebalances) to hands-off (30% leeway, zero rebalances) — the annualized returns barely moved. 10.3% to 10.7%. The difference is pocket change over twenty years.

Now look at the drawdowns. A portfolio rebalanced at a 15% leeway experienced a worst fall of -29.8%. One left to drift at 30% leeway? -36.2%. That's a six-percentage-point gap in how hard the worst crash hits you — and the emotional difference between a drawdown you can endure and one that makes you sell everything at the bottom.

The sweet spot, according to the data, is a 5-15% leeway band — rebalancing only when your allocation drifts meaningfully from target. Infrequent enough that you're not churning. Frequent enough that you're never wildly overexposed when the next crash arrives.

This is the part most people misunderstand. Rebalancing doesn't dramatically improve your returns. In some cycles, the unbalanced portfolio actually comes out ahead — because it let equity run unchecked during a long bull phase. The advantage of rebalancing shows up across multiple full market cycles, and it shows up primarily in how much less you lose during the bad stretches.

And that's where the real value lives. Because smaller drawdowns mean you're more likely to stay invested. You don't panic-sell at the bottom. You don't abandon your SIPs. You don't convert a temporary decline into a permanent loss. The portfolio survives you — which, as we covered in Part 1, is the whole game.

When to rebalance:

- Once a year is enough for most people — pick a date (your birthday, January 1st, whatever) and stick to it

- Or rebalance when your allocation drifts more than 5-15 percentage points from target — the Value Research data suggests this is the sweet spot

- The simplest method: adjust your SIP amounts for a few months rather than selling and triggering tax

I won't pretend rebalancing is easy to do in practice. It means moving money away from whatever just performed well and toward whatever just underperformed. Every instinct says that's wrong. But you're not making a bet on what will do well next — you're restoring a risk level you already decided was right for you. The discipline is mechanical, and that's the whole point.

If managing your own rebalancing sounds like more discipline than you trust yourself with, look at multi-asset allocation funds. These hold equity, debt, and gold in a single fund, and the fund manager rebalances for you — automatically, without triggering tax on every switch. You give up some control over exact allocations, but you gain something more valuable: the guarantee that rebalancing actually happens, even when you're too scared or too busy to do it yourself.

SIPs: Your Built-In Stabilizer

Rebalancing asks you to act deliberately — to override your instincts once or twice a year. SIPs ask nothing. They just keep running.

When you invest a fixed amount every month through a SIP, you're investing consistently regardless of what the market is doing. You don't need to think about whether it's a good time or a bad time. The decision was made once, and it repeats without asking for your opinion.

But SIPs do something else that's less obvious: they naturally slow down portfolio drift.

A lump sum investment in equity grows unchecked during bull markets — pushing your allocation further and further toward equity. SIPs, because they continuously add to both equity and debt in fixed proportions, act as a natural stabilizer. The fresh money keeps pulling your allocation back toward your target without you having to sell anything.

This is one of the underappreciated advantages of SIP investing. It's a rebalancing mechanism in disguise.

If you're investing via monthly SIPs and your allocation drifts, simply redirecting a few months of SIP contributions toward the underweight asset class is often enough to rebalance — no selling, no tax, no agonizing decisions.

When the Screen Is Red and Your Hands Are Shaking

So your portfolio is bleeding. Your thumb is hovering over the "Redeem" button. Before you press it, I want you to sit with a few questions. Not because they'll make the fear go away — they won't. But they'll buy your rational brain a few seconds of airtime before your lizard brain does something expensive.

What was my goal when I started? Pull it up. Write it down if you have to. "₹80 lakh for a house down payment in 10 years." "₹1 crore for retirement in 18 years." The crash hasn't changed your goal. Has it changed the timeline? Almost certainly not. The crash feels urgent. Your goal is measured in years.

Do I know what I own? Can you name your funds? Do you know whether they're large-cap, flexi-cap, small-cap? Understanding what you own reduces anxiety — you're not holding some mysterious thing that might go to zero. You're holding a diversified basket of India's largest companies. They were profitable last year. They'll be profitable next year. The market is just arguing about the price.

Is my allocation drifted or broken? If your 60/40 has drifted to 45/55 because of the crash, that's the market doing its thing — a signal to consider rebalancing, not a reason to panic. If your allocation was 100% small-cap with no debt, the crash is teaching you something important about portfolio construction. And if you need money in 2 years and it's sitting in 80% equity, that's a structural problem the crash has exposed — commit to gradually moving short-term money to debt once markets recover.

Are my SIPs still running? This is the single most expensive thing to stop during a crash. Every cancelled SIP breaks the consistency that makes the strategy work in the first place. If you do nothing else, do this: leave them alone.

Am I making a decision, or reacting? "I've reviewed my allocation and I'm rebalancing per my annual plan" — that's a decision. "I can't take this anymore, I'm selling everything" — that's a reaction. Reactions during crashes almost always cost money.

Am I doom-scrolling financial news? If you're checking your portfolio five times before lunch, you already know the answer. Close the app. Open a book. Call a friend. The market will still be there tomorrow — and it will look exactly the same whether you watch it or not.

A crash survival plan exists for one reason: to prevent feelings from becoming trades.

One more thing worth flagging: there's a difference between "my fund is down" and "my fund has a problem." If there are corporate governance issues, a change in investment philosophy, or the fund manager has been replaced — those are reasons to exit, crash or no crash. A fund that's simply down because the market is down? That's just a market being a market.

If a fund has been consistently underperforming its benchmark and peers for 3+ years — not during a crash, but across a full market cycle — that's worth investigating. A few bad quarters during a broad market decline is noise, not signal.

The Long Game

Here's something I find fascinating about market crashes: they feel like they'll last forever while you're in them, and they compress into footnotes almost immediately after.

I've talked to people who invested through 2008. They remember it was terrifying. They remember the headlines — Lehman Brothers, banks collapsing, the Sensex in freefall from 21,000 to 8,000. But mostly what they tell me is what their portfolio is worth now. And it's a number that makes the entire global financial crisis look like a bad week on a very long chart.

The ones who stayed invested didn't do anything heroic. They just didn't sell. That's it. The bar for getting rich in Indian equity markets has always been astonishingly low: invest regularly, don't quit.

No asset class wins every year. Large-caps lead one year, gold the next, mid-caps the year after. The annual leaderboard is essentially random. But across 10 and 15-year periods, diversified equity has delivered 10-14% annualized returns — through every crash, crisis, pandemic, and tariff war that the world has thrown at it.

The dust always settles. And when it does, the returns hold their ground.

Building Before the Next One

If this is your first crash and you've survived it — or you're in the middle of surviving it right now — I want you to know something: you've earned something that no article, no video, no financial advisor can give you. You've earned experience.

You now know what -30% feels like in your gut, not on a chart. You know which WhatsApp groups make you spiral. You know whether you're the type to check your portfolio five times a day or once a month. You know your own breaking point — or at least you're closer to knowing it.

That knowledge is incredibly valuable. Use it. Before the next crash — and there will absolutely be a next one — build the system:

- Set your asset allocation based on what you can actually tolerate, not what maximizes theoretical returns on a spreadsheet

- Automate your SIPs so the decision to invest was made once, on a calm day, and doesn't need to be remade every month when you're scared

- Pick a rebalancing date and commit to it — your birthday, January 1st, whatever works

- Build an emergency fund that buys you time and choices when the world feels uncertain

- Write down your goals and put them somewhere you'll see them during the next crash

And if you've already exited and you're waiting for the "right time" to get back in — stop waiting. There is no right time. The best day to restart is today. The second best is tomorrow. The worst day is "when things look better," because by then the recovery is already priced in.

The goal here isn't to become someone who feels nothing when markets fall. That person doesn't exist. The goal is to become someone who has built enough structure around themselves that fear doesn't get a vote in their financial decisions.

Wealth belongs to the people who are still invested when the recovery begins — not the ones with the best stock picks or the cleverest strategies.

Related Reading

- When Markets Crash — Part 1 — The psychology of panic and what history teaches us

- Equity Mutual Funds — Part 3: Understanding Risk — Risk fundamentals for SIP investors

- Equity Mutual Funds — Part 4: Building Your Portfolio — Portfolio construction and rebalancing basics

- Basics of Investing — The foundation: insurance, emergency fund, asset classes

Disclaimer: I am NOT a certified investment advisor. This is shared purely for educational purposes. Markets carry risk, and past performance doesn't guarantee future results. Always do your own research.