This article is indicative and general in nature. I am NOT a certified investment advisor. Each of us has individual circumstances — these observations may not be suitable for everyone to follow blindly. This is shared purely for educational purposes.

In every family, there is someone who was careful with money. The person who opened fixed deposits when FDs were the only thing a middle-class Indian trusted. Who paid LIC premiums every quarter without missing one. Who had a PF account from the first job that never got transferred and a second one from the job after that. Somewhere along the way, maybe in the early 2000s, someone talked them into buying fifty shares of Infosys or Reliance. They kept the physical certificates in a brown envelope in the steel almirah. They might have had a PPF. They almost certainly had more than one savings account — the salary account, the one opened for a home loan, the one from the bank near the old house that never got closed.

They did everything right. They saved. They invested. They were disciplined for decades.

And then one day, they were gone.

And nobody knew where any of it was.

The Graveyard of Good Intentions

As of December 2025, ₹2.2 lakh crore in financial assets lies unclaimed across India's institutions. Two lakh crore. That is not idle money parked by the wealthy. That is the accumulated savings of ordinary people — teachers, clerks, engineers, shopkeepers — whose families could not find what was left behind.

The breakdown is worse than the total.

| Where the money sits | Unclaimed amount |

|---|---|

| Bank deposits (RBI's DEA Fund) | ₹97,545 crore |

| Shares and dividends (IEPF) | ₹89,004 crore |

| Insurance proceeds (IRDAI) | ₹20,062 crore |

| Provident fund (EPFO) | ₹10,915 crore |

| Mutual fund redemptions (SEBI) | ₹3,452 crore |

| Total | ~₹2.2 lakh crore |

Behind those numbers: 31.87 lakh dormant EPF accounts. 75 lakh inactive mutual fund folios. 15 lakh shareholders whose shares have been transferred to the government because nobody claimed them. Bank deposits sitting untouched for ten years — not because the owners forgot, but because the owners are gone and the families never knew the accounts existed.

Every rupee in that table was saved by someone who thought they were building something for the people they loved. The savings worked. The communication didn't.

The Five Ways Money Disappears

It is not one catastrophic failure. It is five quiet ones, each of them common enough to be happening in families across the country right now.

1. Nobody knows it exists

A man opens an FD at Indian Bank in 2003 because the branch manager is his friend. He moves cities in 2008. The account stays. The passbook goes into a drawer. The friend retires. The FD auto-renews every year, silently, and after ten years of no activity, the bank transfers the entire amount to the RBI's Depositor Education and Awareness Fund.

That money is technically recoverable. But first, someone in the family has to know it exists.

The same story plays out with old employer PF accounts, insurance policies bought through agents who changed companies, shares held in physical form before demat became mandatory, and PPF accounts at post offices in towns the family left decades ago. Each one invisible unless someone wrote it down.

2. Nominee doesn't mean what most people think it means

This is the single most dangerous assumption in Indian personal finance.

Most people believe that naming a nominee on a bank account, demat account, or insurance policy means the money goes to that person. It does not. The Supreme Court settled this definitively — a nominee is a custodian, not an inheritor. The nominee receives the money in trust and is legally required to distribute it to the rightful heirs under succession law.

A nominee is NOT an heir. Only a registered will determines who inherits assets. Without a will, assets are distributed according to personal succession law — Hindu Succession Act, Indian Succession Act, or Muslim Personal Law — regardless of what the nominee field says. The nominee is just the person the institution hands the money to. What happens after that is a legal question the family will have to answer in court if there's no will.

Without a will, a simple bank account withdrawal becomes a legal process involving succession certificates, court applications, and months of waiting. Multiply that across four banks, two demat accounts, three insurance policies, and a PPF — and the surviving family is spending the first year of grief in government offices and lawyer's chambers.

And when there is no nominee at all — which is far more common than people realise — the process turns into something genuinely cruel.

A family member passes. The family goes to the bank, the mutual fund house, the insurance company. The first question every institution asks: is there a nominee? No. Then the institution freezes the account. Nothing moves until the family produces a succession certificate.

Getting a succession certificate means filing a petition in district court. The court examines it, publishes a public notice in newspapers inviting objections — anyone with a claim has 30 to 45 days to respond. If there are no disputes, the certificate might come through in three to six months. If there are disputes, or if the court is backlogged, it can stretch to a year or more. The family pays court fees, lawyer fees, newspaper publication charges.

And this is per institution. A succession certificate for a bank account doesn't automatically work for a mutual fund folio at a different AMC. Some institutions accept it, some ask for a separate claim process on top of it. For demat accounts, there's a separate transmission procedure. For insurance, a separate claims form with its own documentation trail.

Here is what the process looks like side by side:

| With nominee | Without nominee | |

|---|---|---|

| Bank account | Death certificate + nominee KYC → funds released in 1–2 weeks | Succession certificate from court → 3–12 months, plus court and lawyer fees |

| Mutual funds | Claim form + death certificate + nominee KYC → transmitted in 2–4 weeks | Succession certificate or probated will required; for claims above ₹5 lakh, additional indemnity bond and NOC from all legal heirs |

| Insurance | Claim form + death certificate → settled in 30 days (IRDAI mandate) | Legal heir certificate + affidavit + indemnity bond → months of back-and-forth |

| Demat/shares | Transmission request + death certificate + nominee documents → 2–3 weeks | Succession certificate + transmission form + separate process for each depository participant |

| EPF | Form 20 + death certificate + nominee details → 30 days | Legal heir certificate + employer verification + regional PF office processing → months |

The money doesn't earn interest while it's frozen. The SIPs stop. The insurance lapses. The FD that was meant to fund a child's education sits in limbo while the family fights paperwork. Every institution's process runs on its own clock, and none of them coordinate with each other.

This is what the absence of a nominee actually costs — not just money, but months of a grieving family's time and energy spent proving they are who they say they are.

3. The password dies with the person

A mutual fund portfolio on Kuvera. Stocks in Zerodha. Bank accounts with net banking. Insurance on the LIC app. EPF linked to a UAN that requires an OTP on a mobile number.

The person is gone. The phone is locked. The email has two-factor authentication. The Kuvera login is behind a password nobody else knows. The Zerodha account needs a TOTP from an authenticator app on a phone that's now a black screen.

Every layer of security added to protect money while someone is alive becomes a wall between the family and that money once they're gone. The more digitally organised a person was, the harder it gets — because the institutions are now behind apps, not behind bank counters where a manager could recognise a familiar face.

4. The silent dependency

This is the one nobody talks about.

In millions of Indian households, one person handles all the money. The investments, the taxes, the insurance renewals, the SIP top-ups, the FD rollovers. The other person — usually the spouse — knows money exists but not where, not how much, not in which account, not under whose name. Never logged into the demat. Doesn't know what a CAMS statement is. Couldn't name the mutual fund house if asked.

This isn't negligence. It's how most Indian families operate. One person carries the financial knowledge. The other carries trust.

When the person with the knowledge goes, the person with the trust is left holding nothing but grief and a phone full of apps they've never opened.

And it gets worse. In many families, the person who "handles money" also manages the finances of other family members — the spouse's PPF, the parents' FDs, the children's Sukanya Samriddhi accounts. The accounts are in their names. But the logins, the renewals, the operations — all run through one person. When that person is gone, the family doesn't just lose the inheritance. They lose access to their own money.

5. The bureaucratic wall

Assume the family knows every account, every policy, every folio number. They still face this:

- A death certificate (which takes 7–21 days depending on the municipality)

- A legal heir certificate or succession certificate (which can take months and requires court applications in contested or intestate cases)

- Separate claim forms for every single institution — each bank, each AMC, each insurance company, each PF office

- Indemnity bonds and NOCs from other legal heirs

- KYC re-verification for the claimant

- Transmission requests for demat shares (different process for physical shares)

- For jointly held accounts without "either or survivor" mandates — the full legal heir process even if the co-holder is the spouse

Each institution has its own process. Each process has its own timeline. Each timeline assumes the claimant is not also mourning.

What the Government Built

To be fair, the government has noticed the problem. In the last two years, a set of recovery portals has come online:

| Portal | What it does |

|---|---|

| UDGAM (RBI) | Search for unclaimed bank deposits across all banks; 18.86 lakh registered users |

| MITRA (SEBI) | Trace inactive and unclaimed mutual fund folios across all AMCs |

| IEPF Portal (MCA) | Search for unclaimed shares and dividends transferred to the government |

| e-PRAAPTI (EPFO) | Locate dormant PF accounts without a UAN |

| Bima Bharosa (IRDAI) | Track unclaimed insurance amounts |

In October 2025, the government launched "Your Money, Your Right" — a nationwide campaign to push awareness and reclaims. Within months, ₹2,000 crore had been returned.

These portals are genuinely useful. For families searching for accounts a deceased member may have held, UDGAM handles bank deposits and MITRA handles mutual funds. Both allow PAN-based searches. But they are recovery tools — they help after the crisis. The real fix is upstream.

The Fix Is Simpler Than Most People Think

None of this requires a financial advisor. None of it costs money. It requires about two hours and the willingness to sit with a thought most of us avoid: none of us will always be here to explain.

1. Write a will

A will is not a rich person's document. It is a one-page instruction that tells the legal system who gets what, without ambiguity, without court intervention, without family disputes. A lawyer can draft one for ₹5,000–₹15,000. It needs two witnesses (who are not beneficiaries). That's it.

Anyone with a bank account needs a will. Anyone with a family needs a will. The people who think they don't need one are exactly the people whose families end up in court.

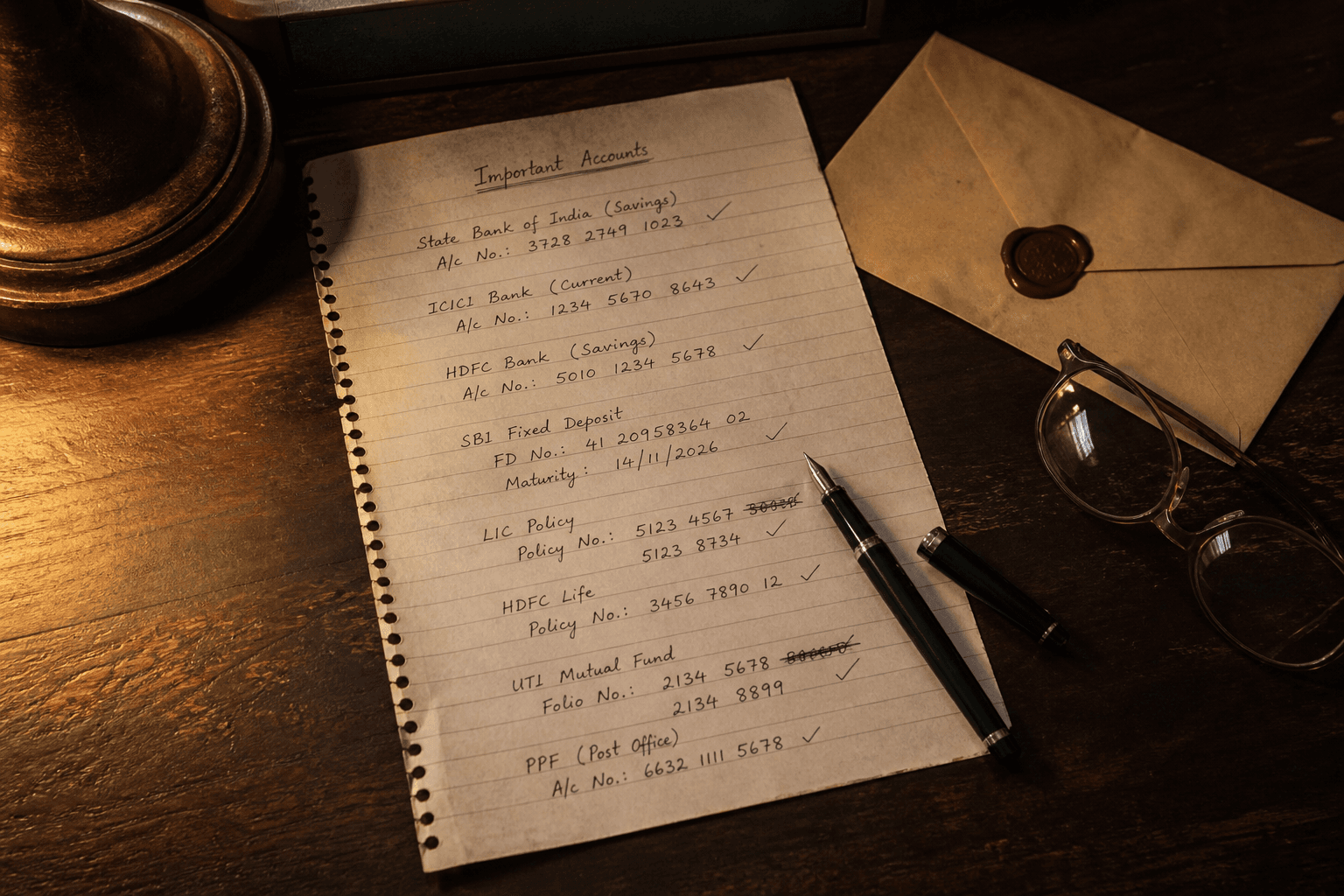

2. Draw the map

This is the idea that Dhirendra Kumar at Value Research calls "the single page" — and he is right that it matters more than any portfolio's XIRR.

One document. Physical or digital (ideally both). It lists:

- Every bank account — bank name, branch, account number, IFSC code

- Every demat account — broker, DP ID, client ID

- Every mutual fund folio — AMC name, folio number

- Every insurance policy — company, policy number, type (term/health/endowment), premium due date

- EPF — UAN, member ID, linked employer

- NPS — PRAN number

- PPF — bank/post office, account number

- Any other investment — bonds, sovereign gold bonds, real estate documents, crypto (if applicable)

- Name and phone number of the financial advisor, CA, or lawyer

- Where the physical documents are kept — "Top shelf, bedroom cupboard, brown file"

What NOT to put on the map:

- Portfolio values (they change weekly and create a false sense of completeness)

- Passwords (those go separately — written down and kept in the household safe place, the same almirah or locker where the family keeps important documents. The family should know it's there. Digitally savvy families can use a shared password manager with emergency access — but a page in a known, safe spot works just as well)

Update the map whenever something changes — a new account, a closed policy, a switched broker, a new SIP. And even if nothing changes, review it once a year. The map is only useful if it matches reality on the day someone needs it.

3. Set nominees on everything

Every account needs a nominee check. Every single one. If a nominee isn't set, set one. If it's an ex-spouse or someone who has passed, update it.

Banks, demat, mutual funds, insurance, EPF, NPS, PPF — every single one. The nominee won't inherit automatically (that's what the will is for), but a valid nominee makes the immediate claim process vastly simpler. Without one, the institution demands a succession certificate before releasing a single rupee.

A nominee is the person who picks up the money. A will is the document that decides who keeps it. Every family needs both.

4. Make sure someone else knows

The map is useless if nobody knows it exists. At least two people — a spouse and one other trusted person (a sibling, an adult child, a close friend) — should know where the map is. Not the details. Just the location.

"There is a document in the Google Drive folder called 'If Something Happens.' It has everything."

"There is a brown envelope in the steel almirah, second shelf from the top. Open it if I'm not here."

That's enough.

5. The hardest one

In every family, there is the person who "handles the money" — for the spouse, the parents, everyone. That person has one more responsibility beyond the map and the will.

Teach someone. Or, at the bare minimum, make sure someone else can step in.

A spouse doesn't need to understand asset allocation. But they need to know which bank their salary account is with, how to log into it, where their PPF is, and who to call if something breaks. Elderly parents don't need to learn Zerodha. But someone other than the one person who manages everything needs to know that the FD is at Canara Bank, Mylapore branch, and it comes up for renewal in October.

The financial dependency that lives in most Indian families is invisible because it works perfectly — until the person holding it all together is no longer there. Then it becomes the thing that breaks everything else.

The Real Cost

The ₹2.2 lakh crore sitting unclaimed across India's financial system is not a failure of regulation. UDGAM exists. MITRA exists. The IEPF portal exists. The government has built the recovery infrastructure.

The failure is upstream. It is personal. It is the conversation that never happened. The page that was never written. The will that was always going to be done "next month." The password that lived in only one person's head. The spouse who was never shown the portfolio — not out of secrecy, but out of the quiet assumption that there would always be time.

Dhirendra Kumar wrote it best: "You have spent decades building something for the people you love. The portfolio is done. The map is not."

The investment is not finished until the people who inherit it can actually find it. The financial plan is not complete until the person who didn't build it can navigate it. The love someone puts into thirty years of disciplined saving means nothing if it ends up in a government fund because nobody knew it was there.

Two hours. A will. A single page. A conversation.

That is all that stands between everything a family has built and the ₹2.2 lakh crore graveyard.

This weekend. Not next month. Not after the next appraisal. Not when things settle down. This weekend.

Because the one thing a portfolio cannot do — the one thing no SIP, no term plan, no diversified equity fund can ever do — is explain itself after the person who built it is gone.